132 / 316

132 / 316

AfrAsia Bank Limited and its Group Entities

Annual Report 2015

page 130

MANAGEMENT DISCUSSION AND ANALYSIS (CONTINUED)

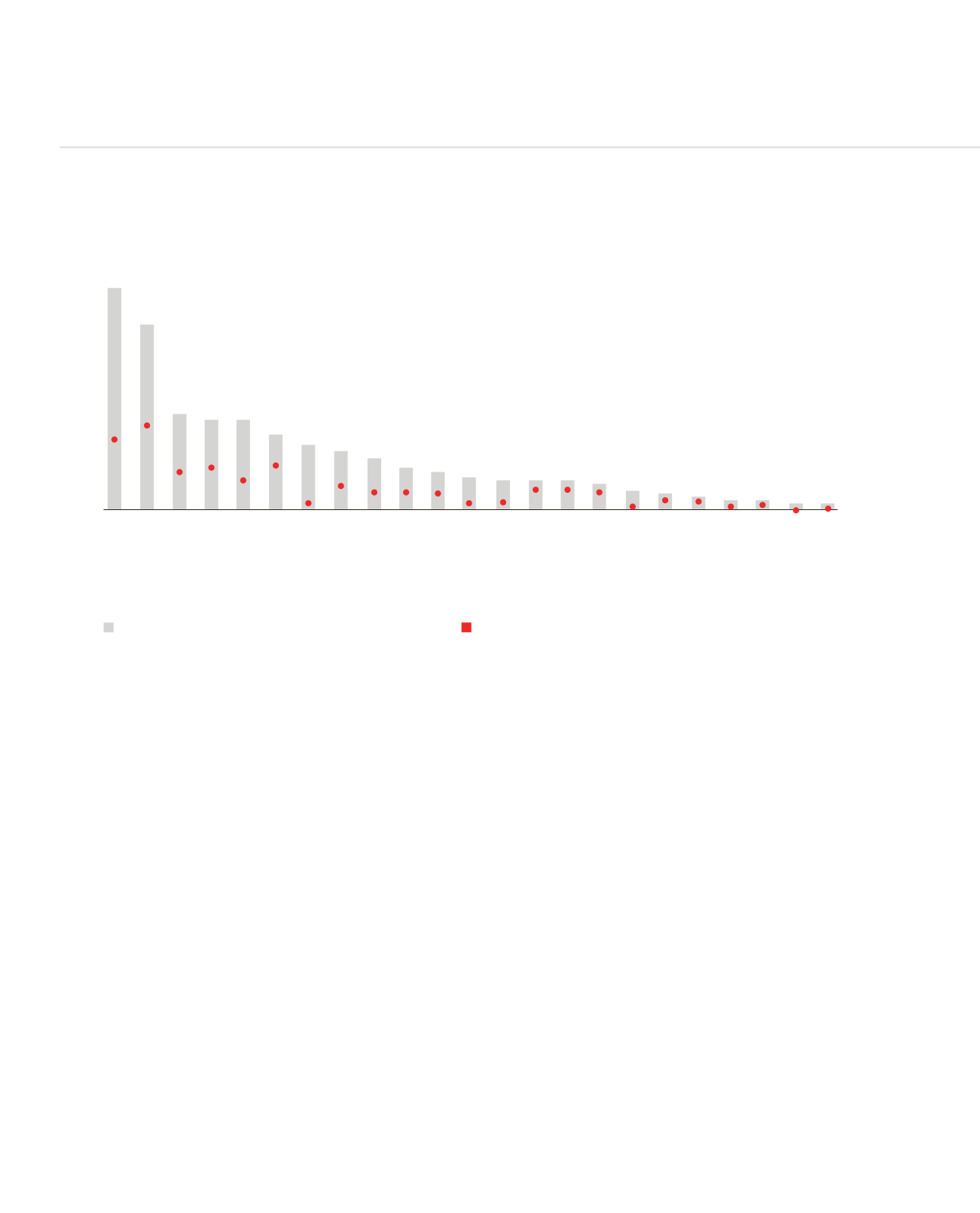

Commodity revenue windfall gains enjoyed by resource-rich countries (2002–2015): Sharp declining trends.

Source: “How to manage the commodity roller coaster,” Huff Post, 10 July 2015

Prospects within the euro area

Following the crisis in Greece in early August 2015, the euro area has showed timid signs of recovery amidst lacklustre medium-term

outlook. The support to recovery seemed to be based on weak fundamentals: cheaper oil prices, monetary easing and a weaker euro.

In 2016, growth is expected to reach 1.6%, up from the expected 1.5% in 2015. Downside risks, including stagflation, would tend to prevail

in the medium term, and could possibly extend to 2020.

Emerging economies: Can India’s Elephant take over from the Chinese Dragon?

The size of Asia’s third largest economy, India, is only one-fifth that of China. It is therefore unlikely to be able to provide much support to

global growth of the same order of magnitude as China, which has been acting as the most stable contributor to world economic growth.

Political acrimony is also the order of the day in India, despite Narendra Modi’s landslide victory in 2014, which had fuelled hopes of a

speedy recovery. Long outstanding reforms also seem to be lacking, which could prevent India from fully capitalising on its northern

neighbour’s deepening economic slowdown. Structural reforms remain critical especially in labour markets, the banking sector, tax regime

and land management.

COMMODITY REVENUE WINDFALL

Angola

Kuwait

Saudi Arabia

Oman

Congo

Republique of

Kazakhstan

Brunei

Darussalam

United Arab

Emirates

Algeria

Russia

Bahrain

Nigeria

Gabon

Bolivia

Trinidad and

Tobago

Ecuador

Suriname

Zambia

Niger

Peru

Colombia

Cameroon

Botswana

o

50

100

150

200

250

300

Commodity Fiscal Revenue Windfall (2012 versus 2002)

Commodity Fiscal Revenue Windfall (2015 versus 2002)