117 / 316

117 / 316

AfrAsia Bank Limited and its Group Entities

Annual Report 2015

page 115

MANAGEMENT DISCUSSION AND ANALYSIS

ECONOMIC OVERVIEW AND OUTLOOK

The Domestic Landscape – Review of 2014/15

2014 elections: A landslide signaling sweeping reforms

On 17 December 2014, a new coalition Government was sworn in after winning a spectacular and unexpected landslide victory

in the general elections. This brought an end to nine years of power led by the Labour Party and signaled the beginning of a new

economic agenda, which was the hallmark of the electoral campaign. After months of uncertainties and stalled policy action which

are often characteristics of any democratic pre-election period, the new Government took office with the promise that it would bring

a “second economic miracle” to the shores of Mauritius.

Whilst the first few months have been characterised by what some would term as “populism” and others “interventionism,”

the country is now “at the crossroads” (which was the title of the first Budget presented by the new team), faced with new realities on

the ground, the most important being the threat of a “middle-income trap” and growing disparities in income levels and distribution.

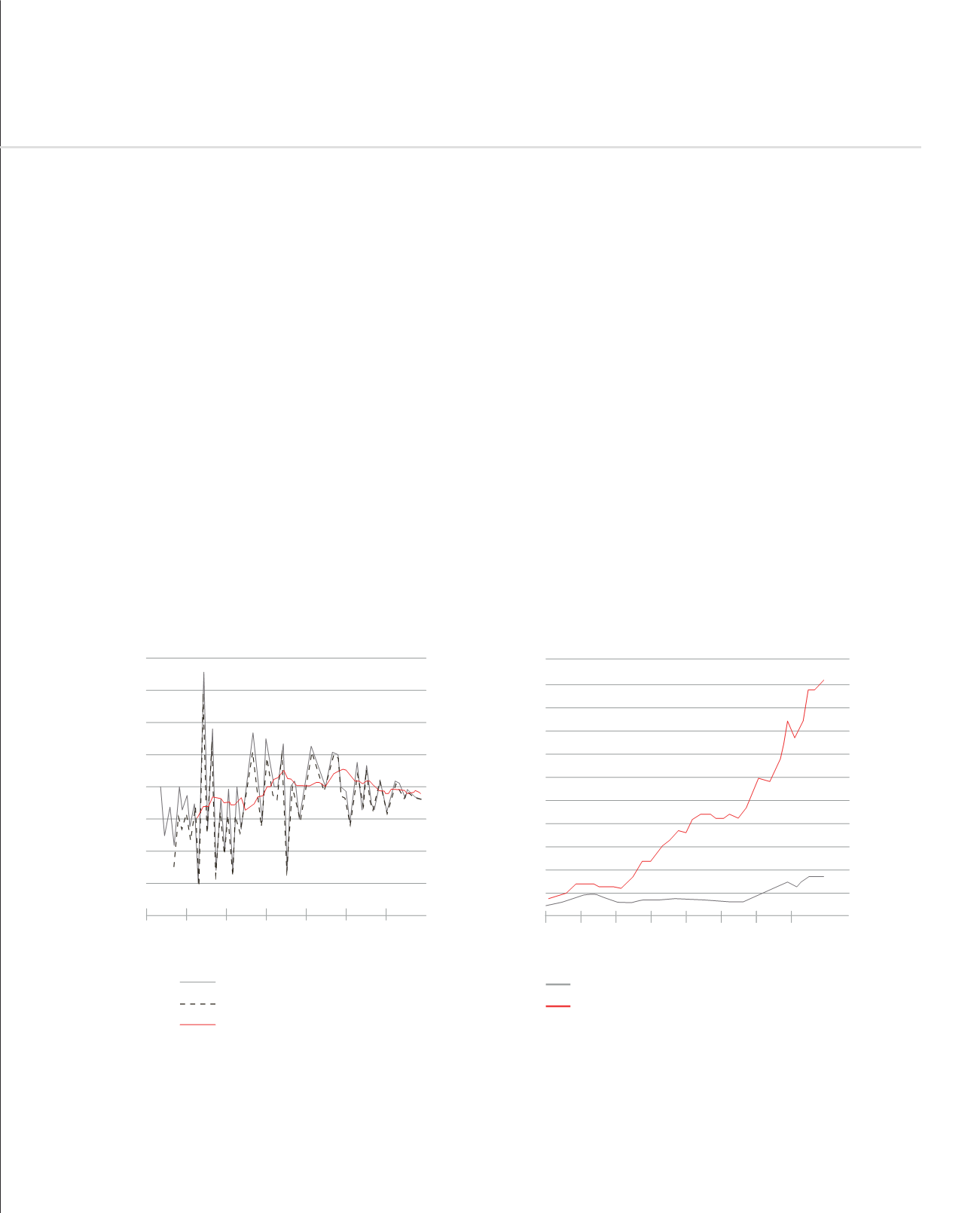

GROWTH AVERAGED 5% OVER THE

LAST DECADES AND AVERAGED 4% LATELY

25

20

15

10

5

0

-5

-10

-15

1950

1960

2010

2000

1990

1980

1970

Real growth

Real growth per capita

10-year MA

8,000

7,000

9,000

10,000

6,000

5,000

4,000

3,000

2,000

1,000

0

1975

1980

1985

1990

1995

2000

2005

2010

GDP/Capita (USD): Mauritius

GDP/Capita (USD): SSA

%

USDPER-CAPITA INCOME ROSE RAPIDLY, PUTTING MAURITIUS

FIRMLY IN HIGH MIDDLE INCOME STATUS

Pictorial representation of what Mauritius calls its ‘first economic miracle’

Source: Systematic Country Diagnostic, World Bank Group, June 2015