Download Investor Relations App

| |

|

|

Download Investor Relations App

|

|

|

ANNUAL REPORT 2015

| |

|

|

|

|

|

Click or Scroll for more

employees

customers

Acquisition of

in shareholding of AfrAsia Bank Limited by the National Bank of Canada

hours dedicated to social and environmental programmes

GENDER

female

male

WHERE WE HAVE CLIENTS

countries

ORDINARY DIVIDENDS PER SHARE (BANK)

children supported in Mauritius through our CSR programmes

TRAINING

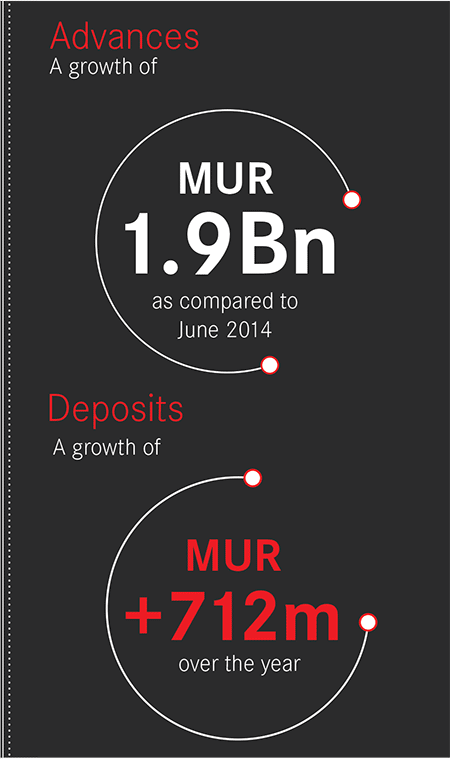

LOANS & ADVANCES (BANK)

DEPOSITS (BANK)

Adhering to sustainability reporting policy, UN Global Compact

AfrAsia Bank Limited holds a Banking Licence to conduct banking business in Mauritius issued by the Bank of Mauritius under Section 7 of the Banking Act 2004 since 29 August 2007. The Bank and its Group Entities have also been granted the following licences:

| Legal Entity | Domiciled | Regulatory Oversight |

|---|---|---|

| AfrAsia Bank Limited | Mauritius (Domestic) | Bank of Mauritius, Financial Services Commission, South African Reserve Bank |

| AfrAsia Holdings Limited | Mauritius (GBL1) | Bank of Mauritius, Financial Services Commission |

| AfrAsia Corporate Finance (Pty) Limited | South Africa | South African Reserve Bank, Financial Services Board (FSB-South Africa) |

| AfrAsia Corporate Finance (Africa) Limited | Mauritius (GBL1) | Financial Services Commission |

| AfrAsia Capital Management Limited | Mauritius (Domestic) | Financial Services Commission |

The Bank of Mauritius has also granted the Bank the status of Primary Dealer to deal in government securities.

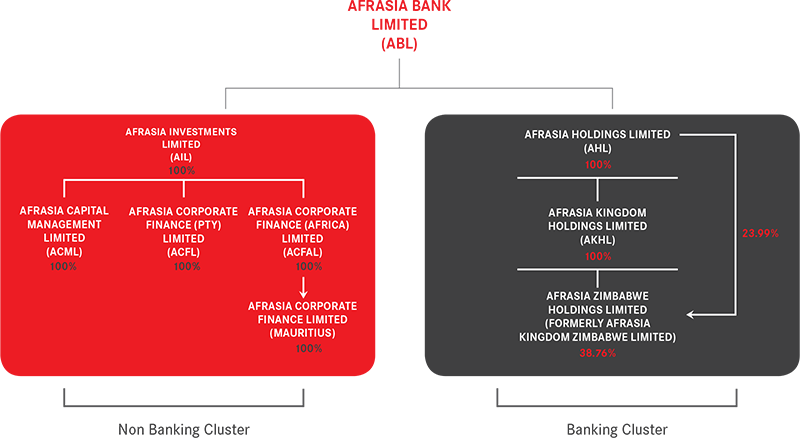

| HOLDING COMPANY | |

|---|---|

| AfrAsia Bank Limited | |

| Subsidiaries /Associates | |

| AfrAsia Investments Limited | 100% |

| AfrAsia Holdings Limited | 100% |

| AfrAsia Kingdom Holdings Limited | 100% Effective as from 18 February 2015 |

| AfrAsia Corporate Finance (Pty) Limited | 100% Effective as from 1 October 2013 |

| AfrAsia Corporate Finance (Africa) Limited | 100% Effective as from 1 October 2013 |

| AfrAsia Capital Management Limited | 100% Effective as from 3 October 2013 |

| AfrAsia Kingdom Zimbabwe Limited (Formerly Kingdom Financial Holdings Limited) | 62.75% Effective as from 18 February 2015 |

|

|

|

|

Please hover on image for information

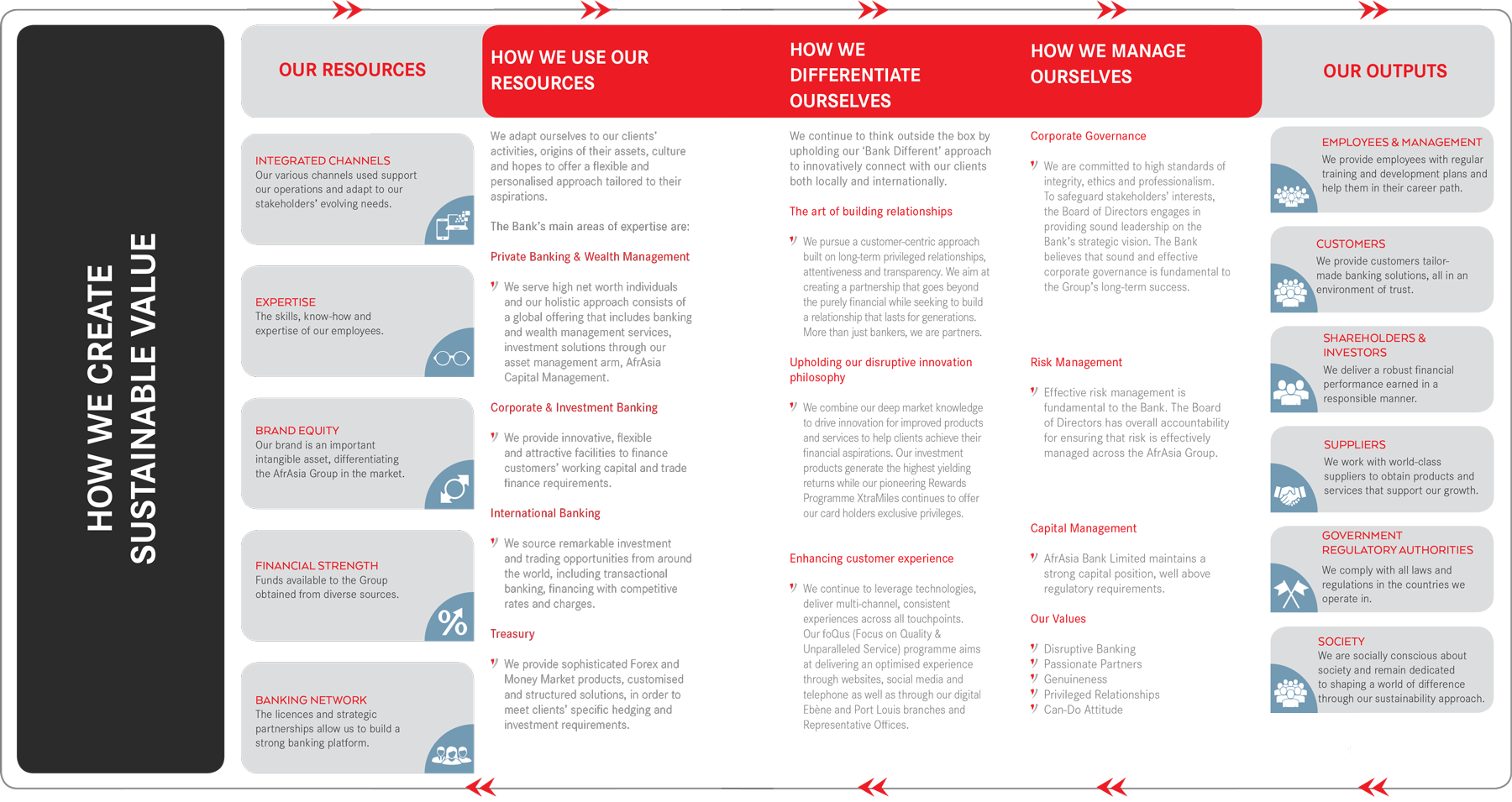

Diversification across Africa, Asia and the World

The Bank continues to build on its relevance locally, regionally and internationally through its offices in Mauritius (Port Louis and Ebène), South Africa & the United Kingdom. The Bank keeps on exploring opportunities in core African markets, expanding its presence in the SADC and COMESA regions, across Asia and Europe as well as emerging markets while developing its tailored banking services to a wider market.

Building a Culture of Excellence

The Bank's unique culture is fundamental to who we are as an organisation and a key aspect of its brand promise, 'Bank Different'. With a passionate team serving clients in more than 121 countries, the Bank continues to build a talent pipeline to ensure that its workforce is representative of its niche markets and clients' aspirations.

Corporate & Investment Banking, Private Banking & Wealth Management, International Banking and Treasury

AfrAsia Bank Limited continues to meet clients' evolving needs to differentiate itself in its target market through its value proposition and remains a strong competitor in its core business segments.

Taking the AfrAsia brand internationally

From enhancing customer experience to launching innovative banking solutions, AfrAsia Bank Limited has always been recognised for revolutionising the financial sector, thus creating value for its customers while responding to their specific needs and financial aspirations. The Bank aims at continuously shaping its commercial tactics to improve operational processes, putting a greater focus on its core business segments and integrating multi-channel strategies to create lasting relationships and reinforce customer loyalty while simultaneously consolidating the Bank's positioning locally, regionally and internationally

Our client-centric approach, diversified business model and commitment to our long-term strategic priorities have been fundamental to our growth and will allow us to continue to create value for all stakeholders

To achieve a sustainable rate of return on equity above the Bank's cost of equity capital

To be the best private and corporate bank in Mauritius

To be a leading provider of innovative banking solutions in our core business segments, serving the Africa-Asia trade corridor and beyond

To create a homogenous brand experience and consolidate the Bank's local, regional and international position

To identify and develop talent to guarantee success while fostering pride in belonging to the Bank

To penetrate new markets and fully realise opportunities to drive investment, trade and wealth creation

Our values deserve an award, come to think of it, more than one. Clients have always been a touchstone for AfrAsia Bank Limited. A strong commitment to client satisfaction is what drives the Bank. Its hard work, conviction, trust, enthusiam and devotion together with the most loyal clientele, have built a rock-solid foundation for award-winning service and performance.

‘Best Transport Infrastructure Deal in EMEA’ for supporting the Ethiopian Railways Corporation’s rail infrastructure upgrade

Best Wealth Management Provider in Mauritius 2014

| STAKEHOLDER GROUP | HOW WE ENGAGE WITH OUR STAKEHOLDERS | THEIR CONTRIBUTION TO VALUE CREATION | WHAT OUR STAKEHOLDERS EXPECT FROM US | WHAT CONCERNS OUR STAKEHOLDERS |

|---|---|---|---|---|

| EMPLOYEES AND MANAGEMENT |

|

|

|

|

| CUSTOMERS |

|

|

|

|

| SHAREHOLDERS AND INVESTORS |

|

|

|

|

| SUPPLIERS AND SERVICES |

|

|

|

|

| GOVERNMENT REGULATORY AUTHORITIES |

|

|

|

|

| SOCIETY |

|

|

|

|

Please hover on year for more

Keep on innovating to provide a different banking experience to our clients locally, regionally and globally

Pursue balanced growth opportunities and efficient use of capital to create more value for our stakeholders in the long-term

Extend our presence and product offering into our key markets, primarily into Africa and Asia, while capitalising on shareholders' expertise in those markets

Refine our risk appetite across our diversified business model while consolidating strong risk management culture

LIM SIT CHEN LAM PAK NG

Chairman

This report marks many milestones achieved this past year and numerous new avenues forward for AfrAsia Bank Limited. It is the first report to you from an Independent Non-Executive Chairman, which duty I have been entrusted with. It is with humility and a deep sense of service that I have accepted to be the second Chairperson of your Bank.

On behalf of the Board and the Bank, we place on record our sincere thanks and deep appreciation of the contribution and leadership of Arnaud Lagesse, CEO of GML, the founding and largest shareholder of AfrAsia Bank Limited. Arnaud served as Chairman for the first seven years, overseeing the creation and success of the Bank along the visionary lines he aspired to it when fi rst seeking the banking licence in 2006.

I welcome the new CEO, Sanjiv Bhasin, who will be tasked to spearhead the reorganisation of the Bank's internal structure to better serve our clients while reinforcing our footprint in key markets and creating more value for all stakeholders.

Allow me to comment briefly on the performance of the Bank for the year ended 30 June 2015.

I would like to emphasise that the Bank has been profitable and has a strong capital base. Offsetting strong net interest income growth and treasury dealing profits was the residual impact of closing the Zimbabwe banking operations in February 2015.

The net result was thus heavily impacted, with Bank net profit after tax at MUR 175m vs MUR 223m last year and Group net loss after tax at MUR 176m vs Group net profit after tax of MUR 325m last year. With the strategic investment by National Bank of Canada, now at 17.5% along with a general rights issue, which in total increased equity capital by nearly MUR 1bn, we now have a strong common equity Tier 1 capital ratio of 7.5% and total capital adequacy ratio of 13.7%. We have maintained all dividend requirements to our Class A shareholders throughout.

Fully aware of the importance of maintaining an adequate level of capital to support further profitable growth, we have adopted a dividend policy that ensures first the payment of dividends to our Class A shareholders; and a flow of dividend payments that provides an adequate cash return to our ordinary shareholders whilst keeping a sufficient amount of retained earnings to fuel the Bank's growth.

The Bank has been a fast growing, dynamic and entrepreneurial business for several years now. At the same time, there has been a focus on fostering a culture that knows of and implements compliance to the regulated environment we operate within. The Bank has also implemented extensive systems, along with significant new executive hires in audit, legal and compliance. Several independent examinations and audits have also been commissioned throughout the year.

The Bank is now operating across many jurisdictions and with substantial numbers of new staff hired over the last years. It is in the process of rolling out a new team culture programme with detailed training and induction programmes. The 'Bank Different' culture has been core to the Bank's success and it is now time to refresh and revalidate how this works in our daily service to customers and how we engage with each other. The Bank has gained and will maintain a competitive advantage from its unique and internally-developed process, which is always a work in progress and the quality, diversity and adaptability of its human resources in an ever-changing competitive environment.

Indeed the environment is in constant change. Major trends are already reshaping the global economy. The centre of gravity of the global economy is irreversibly moving to the Africa–Asia axis, coupled with the urbanisation of population in Asia and Africa as a new middle class of consumers emerges; and the disruption of industries with the progress and innovation in the information, communication and technology sector. Your Bank is well-positioned to ride on the waves of these trends.

The Bank will leverage on the key attributes of its four main shareholders, namely the entrepreneurial spirit and mind-set of its major and founding shareholder, GML Group, to offer a unique suite of banking services to the family owned business and their founders of Africa; the banking and risk management skills of the National Bank of Canada, to offer sector specific financing and risk management solutions to companies in the region, with an emphasis on Africa; the network of the investee companies of PROPARCO to expand the Bank's network of collaboration in Africa and the business network in Africa and Asia of Intrasia Capital to develop new business relationships.

The Bank has now reached a level where it can count on a stable stream of profitability and cash flow. It is well equipped to forge ahead and assume a greater responsibility in society that transcends its primary objective of profit maximisation for its shareholders.

We shall continue to ensure that the Bank achieves a target return on average equity capital commensurate with the risk inherent to our banking franchise. This will require that the Bank clearly defines its risk appetite and then judiciously deploys its capital to maximise the return on its capital according to this risk parameter.

AfrAsia Bank Limited continues to incorporate sustainability approaches to the way it conducts business. Across society, the workplace and the communities it serves, the Bank embraces Environmental, Social and Governance considerations (ESG) to align with its corporate strategy and uphold its sustainability structure.

On a deeper level, the Bank will ensure that each and every member of its staff becomes fully conscious and aware of being a Human Being and not just a Human Doing. While the Bank fully assumes its responsibility as a corporate citizen, it is equally important that the business and regulatory environment remain supportive.

It is a great concern that the Centre's reputation has been recently affected. This now requires the full effort of all members of the financial centre ecosystem to work together to improve our international image.

Fully aware that banking is a highly regulated industry, we fully support all efforts that enhance the reputation of the Mauritius financial centre as a well-regulated and supervised jurisdiction with independent regulatory institutions. However, it is imperative that Mauritius maintains its competitiveness by keeping the cost of compliance at a reasonable level. We are thus proponents of a risk-based approach to supervision and in effective collaborations between the regulator and industry participants in the development of regulation and supervision guidelines. Mauritius is an emerging financial centre focused on serving the banking and capital raising needs of Africa. There is a need to take into account the specific environment of our region in crafting the regulatory and supervisory framework. Otherwise there is a risk of creating road blocks to its development and rendering the centre less competitive.

In the course of the year, one independent director, Mike Pike, retired as per the current banking regulation, having served the seven years. We thank him for his contribution.

I also extend my heartfelt gratitude to James Benoit and Kamben Padayachy who resigned from their respective posts of Chief Executive Officer and Deputy Chief Executive Officer, Head of Global Banking, Treasury & Markets, for their helpful contribution and strategic direction throughout their journey at the Bank. I would also like to thank, Thierry Vallet, Acting CEO for his leadership during the transition period.

On behalf of the Board, I thank you, valued shareholders, who have entrusted us with your capital. I assure you that both the Board of Directors and the entire management team will continue to be prudent stewards of this capital.

I also thank the management and all the staff for their continuing dedication to the building of a 'Bank Different' in the region.

LIM SIT CHEN LAM PAK NG

Chairman

THIERRY VALLET

Acting Chief Executive Officer

It is my honour to present to you the 2015 Annual Report as acting CEO during the transition period between James Benoit and his successor, Sanjiv Bhasin.

James Benoit, co-founder of AfrAsia Bank Limited and who served as CEO since inception, resigned from his position this year. A firm believer of the growth prospects of Africa, James helped to achieve many tangible brand and investor targets regionally and internationally with a uniquely loyal and dynamic team and banking culture. I would like to extend my heartfelt gratitude to him for his contribution. I am also pleased to welcome Sanjiv Bhasin who has an extensive experience of 38 years across market-leading institutions and will continue building on the Bank's success and write the Africa sequel.

This year is a year of transition, not only for AfrAsia Bank Limited, but for Mauritius and beyond. The global economy remained volatile and perplexing during the year. Here in Mauritius, we also had political changes and some corporate failures. These have had their knock-on effects on the economy and for us at AfrAsia Bank Limited. Still, it was the year in which we gained great insight into our business model, continued to innovate and made some inspiring and bold moves.

Our challenges in our Zimbabwe operations continued and we took the decision in February to surrender our banking licence there and wind up the operations. This was expensive financially and painful for the impact on staff there; we have a separate insight on this elsewhere in the report. We also learned though that despite the global turmoil, Africa remains a beacon of investment and AfrAsia Bank Limited is participating strongly in this.

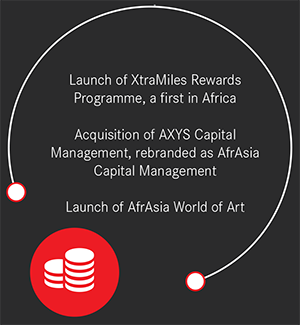

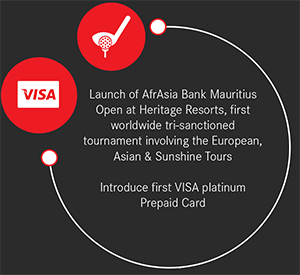

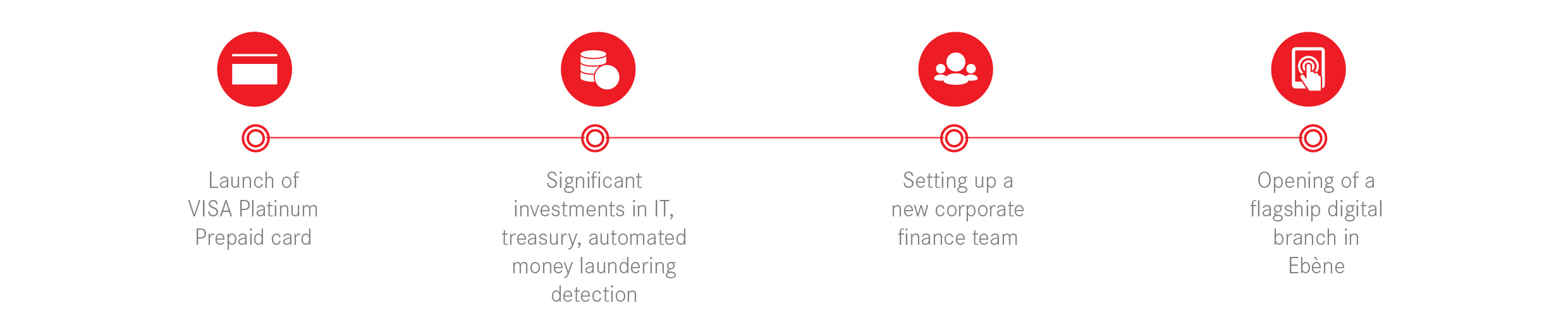

Our uniquely innovative flagship digital banking centre was launched this year along with a prepaid VISA Platinum card; both firsts in this market. Several new investment funds and private banking services were also rolled out. All of these have continued to see us nominated for, and win, international awards yet again.

We brought in National Bank of Canada as a shareholder during the year for an initial 9.5% stake which has since risen to 17.5% on our last rights issue and saw us raise nearly MUR 1bn of fresh Tier 1 capital. We also invested heavily in our brand and we hosted the world's first ever tri-sanctioned professional golf event involving the European, Sunshine and Asian Tours, the AfrAsia Bank Mauritius Open. With the support of the government and other private sector partners, this was the country's largest ever sporting event showcasing just what we can all do together and gave Mauritius and AfrAsia Bank Limited truly global branding coverage.

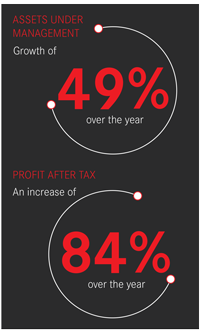

Our asset base stood at MUR 22bn at year end while our liabilities amounted to MUR 67bn. Mainly this was on the back of strong global business and private client deposit flows which increased by over 50%. With clients in over 121 countries, AfrAsia Bank Limited and Mauritius as a jurisdiction are now key financial intermediaries for the entire world that is doing business in Africa and Asia.

We cautiously expanded our loan book at a less rapid pace. With credit market fragility globally and locally and the uncertainty of interest rates and currency wars, this is a deliberate strategy. Our surpluses have largely been deployed in shorter term bank placements and money market lines which provide us more agility to manage balance sheet risks.

The 'Management Discussion And Analysis' discusses the detailed metrics. Total Operating income was strongly up 40% but, with final Zimbabwe write downs, our Net Profit After Tax (NPAT) reduced to MUR 175m. However our core customer loan book has performed well and we have avoided many international and local credit issues that have ensnared our competitors. Cost income ratio remains very well managed despite the heavy investments in people, premises and products.

During the year, we made substantial investments in new IT systems including core banking, treasury, automated money laundering detection, prepaid cards and the new digital branch and office spaces in Ebène. We are now poised to leverage these for several years.

Heavy investment was also made in marketing of, which AfrAsia Bank Mauritius Open was the largest. With our international reach and now that we are part of the largest domestic banks, we can say that AfrAsia as a brand and a business is now well established and winning all manner of international accolades, which then turn into deep business referrals and relationships.

Our total staff headcount increased to 234, with excellent gender diversity of 52% female. Out of the Executive Committee, four [31%] are female and hold vital roles as Head of Marketing, Credit, Finance and Human Resources.

I remain firmly convinced that the strong African investment trends we are seeing will continue. AfrAsia Bank Limited and Mauritius are uniquely equipped to be the key capital and liquidity solutions providers for these investors. This should drive our growth at similar levels for several more years to come. As such, with our new partners from Canada and our continued building of the brand, our people and infrastructure in Mauritius, we have gained insight, remain innovative and are inspired to pursue our strategy.

As a public company incorporated on 12 January 2007 and holder of a Banking Licence issued on 29 August 2007, AfrAsia Bank Limited remains guided by the principles issued by the Mauritius Financial Reporting Council in its "Guidelines on Compliance with the Code of Corporate Governance" by the Bank of Mauritius in its "Guidelines on Corporate Governance" and by the provisions of the Mauritius Companies Act 2001.

Appointed Director: 12 February 2007

Appointed Chairman: 12 February 2015

Qualifications:Qualifications: MBA degree from the Graduate School of Business of Columbia University, New York, N.Y, USA

Lim Sit Chen (Maurice) is the founding partner of Stewardship Consulting, based in Singapore, providing strategy consulting services to family-owned companies and government organisations. Prior to Stewardship Consulting, Maurice was in banking, advising public and private sector clients in treasury and risk management, financial strategy and investment management. He has worked in London, Montreal, New York, Singapore and Tokyo.

A Mauritian and Canadian citizen, born in 1947, he lives in Singapore.

Committees:Board of Directors (Chairperson)

Risk Committee

Corporate Governance Committee

(Chairperson)

Appointed: 31 May 2007

Resigned: 23 September 2015

Qualifications:Chartered Financial Analyst

James was previously a global management executive with the Hong Kong and Shanghai Banking Corporation Group for 16 years in emerging and developing markets in China, Philippines, Hong Kong, the Middle East, Canada and Mauritius. He has developed, implemented and grown leading consumer banking, wealth management, credit card and corporate banking businesses in these regions with proven ability to engage customers, regulators and staff from diverse backgrounds. He is also a co-founder of the local Chapter of the CFA Institute which has won global awards for revitalisation under his Presidency. He is a sought-after financial conference speaker and opinion leader published in media channels in South Africa, India, UK, Vietnam, Singapore, Philippines and Mauritius. James Benoit is not a director of any listed company in Mauritius.

Committees:Board of Directors

(Resigned 23 September 2015)

Risk Committee

(Resigned 23 September 2015)

Conduct Review Committee

(In Attendance up to 23 September 2015)

Audit Committee

(In Attendance up to 23 September 2015)

Corporate Governance Committee

(In Attendance up to 23 September 2015)

Appointed: 27 January 2010

Qualifications:Chartered Accountant(South Africa)

Prior to moving to Mauritius, where he has been for thirteen years, Brett spent fifteen years living in London during which time he was involved in the development of Equitas, the vehicle set up by Lloyds of London to acquire distressed re-insurance contracts. He then founded and built a successful venture capital business focused on the IT industry, ultimately culminating in the listing of companies on the London Stock Exchange, Finnish HEX exchange and exciting other investments via trade sales. Brett is Executive Chairperson of Brait (an investment business listed in Luxembourg and the JSE), an entity incorporated in Mauritius which he joined in 2004. He also sits on the Boards, in a nonexecutive capacity, of a number of privately and publicly-owned investment businesses.

Committees:Board of Directors Audit Committee

Appointed: 12 January 2007

Qualifications:Chartered Accountant(Scotland)

Jean acquired experience in the field of Merchant Banking with Kleinwort Benson in Australia between 1984 and 1991 before joining the Swan Group in 1992. He retired as Chief Executive Officer of the Swan Group in December 2006. He is a Director of a number of companies involved in various economic activities such as finance, tourism, agriculture and commerce in Mauritius and in the region. Four of those companies are listed on the Stock Exchange of Mauritius. He was the Chairperson of the Stock Exchange of Mauritius from 2002 to 2006 and is a member of a number of Corporate Governance and Audit Committees.

Committees:Board of Directors

Audit Committee (Chairperson)

Conduct Review Committee

Appointed: 8 February 2011

Qualifications:Chartered Accountant(South Africa)

Catherine, a Mauritian citizen, holds a Bachelor of Accountancy degree from the University of the Witwatersrand, Johannesburg, South Africa and has been a member of the South African Institute of Chartered Accountants since 1992. She then joined the investment banking industry and has held senior positions in corporate and specialised finance for Ridge Corporate Finance, BoE NatWest and BoE Merchant Bank in Johannesburg. She returned to Mauritius in 2004 to join Investec Bank where she was Head of Banking until June 2010. Catherine is a Fellow Member of the Mauritius Institute of Directors and is currently working for her own account as a Financial Advisor. She is a non-executive director of a number of public and private companies in Mauritius. Catherine McIlraith is a director of one listed company in Mauritius.

Committees:Board of Directors

Audit Committee

Risk Committee

Conduct Review Committee

Appointed: 1 November 2013

Qualifications:ESSEC – Ingénieur Telecoms – MBA Cranfield University (UK)

Nicolas Weiss is a Telecommunications engineer. He is an Essec Business School graduate and holds an MBA from Cranfield (UK). Nicolas Weiss started his career in 1988 at Deltabanque, where he developed an interest rate risk management system. He later developed portfolio insurance and market arbitrage models. In 1991, he joined M.Philippe Oddo and helped raise the clientele of Institutional Investors for mutual funds actions, bonds and derivatives. In 1993, he joined Mr. Le Baron Edmond de Rothschild and was General Manager and Shareholder to the creation of AssMgt subsidiaries of the Rothschild Group in Europe: Rothschild Asset Management (EUR20bn), E.de AssMgt Rothschild Investment Services (USD4bn), and Rothschild Multi Management (EUR5bn). Nicolas Weiss was also director and treasurer for 'Rothschild Fundations' since 1997. He left the Rothschild Group in 2010 to settle in Mauritius. Nicolas Weiss has been teaching finance at ESSEC, at Paris Dauphine and at Arts et Métiers. He is a jury member at ESSEC since 1987.

Committees:Board of Directors

Corporate Governance Committee

Appointed: 14 February 2011

Resigned: 23 September 2015

Qualifications:Master's degree in Monetary Economics from the University of Paris Dauphine and a post-graduate degree in Banking and Finance

Kamben was one of the Founding Executives of AfrAsia Bank Limited since its inception in May 2007. He has over 20 years' experience in banking, having successively worked with BNP Paribas (BNPI), Barclays Bank and Standard Bank prior to joining AfrAsia Bank Limited. He has held senior management roles at both retail and corporate levels throughout his career and has originated investment banking transactions from debt capital markets to structured trade finance. Kamben was the Deputy CEO and Head of Global Banking, Treasury and Markets at AfrAsia Bank Limited. He is a Director of AfrAsia Special Opportunities Fund, a company listed on the Stock Exchange of Mauritius.

Committees:Board of Directors

(Resigned 23 September 2015)

Appointed: 28 October 2011

Qualifications:Fellow of the Association of Chartered Certified Accountants

Born in 1963, Jean-Claude was appointed as Alternate Director to J. Cyril Lagesse in June 2007 and as Non-Executive Director in October 2011. He joined GML in 1997 and is presently the Chief Financial Officer of GML Management Ltée. He is the Chairperson of Phoenix Beverages Limited and of Anahita Estates Limited. He is also Director of a number of companies including LUX Island Resorts Ltd, Alteo Limited and Abax Corporate Services Ltd. Jean-Claude is a director of three listed companies on the Stock Exchange of Mauritius.

Committees:Board of Directors

Appointed: 16 August 2011

Qualifications:FAICD (F) - Australian Institute of Company Directors, MAIE (M) Australian Institute of Energy

Educated in Sydney, Australia, Graeme has lived in Southeast Asia since 1972 and has been responsible for pioneering the development and managing internationally world class mining, energy and infrastructure operations. He is a recipient of the ASEAN Development and the Millennium 500 Awards in 1996 and 2000 respectively for his contribution to growing significant commercial operations in developing nations in Asia. Graeme is the Chairperson and owner of Intrasia Capital Pte Ltd, a private investment group in Singapore and its subsidiaries, including Vita Rice Limited developing healthy rice production in Mauritius. He is also Chairperson of listed companies Intra Energy Corporation and NuEnergy Gas Limited for coal mining and gas extraction. His companies operate extensively in Eastern Africa in coal production and supply, electricity generation, drilling and domestic gas development. Graeme is a humanitarian with interests in poverty alleviation and health improvement. He is a personal Advisor to the Vice Prime Minister and Minister of Energy and Public Utilities in relation to the energy future of Mauritius. He is not a director of any company listed in Mauritius.

Committees:Board of Directors

Appointed: 15 January 2015

Resigned: 1 September 2015

Qualifications:Master's degree in Management and Finance from the "Ecole Superieure de Gestion et Finance" Paris, France

Laurent de la Hogue was appointed Director of the Company in January 2015. Born in 1975, Laurent holds a Master's degree in Management and Finance from the 'Ecole Supérieure de Gestion et Finance' Paris, France. He joined GML in 2001 as Treasurer for the setting up of the Central Treasury Unit and is presently Finance Executive - Corporate and Treasury for GML Management Ltée. Laurent is currently the Chairman of GML Trésorerie Ltée and also Director of a number of companies including Abax Holding Ltd, Forward Investment Development Enterprises Ltd, LUX Island Resorts Ltd, and The United Basalt Products Ltd.

Committees:Board of Directors

Appointed: 16 January 2015

Qualifications:ESSEC

Yves Jacquot has wide experience in the banking sector. He is currently the First Vice-President of International Development for the National Bank of Canada Group and the Deputy Chief Executive of NATCAN INVESTISSEMENTS INTERNATIONAUX SAS which is a subsidiary of National Bank of Canada. Previously, he was the Deputy Chief Executive of BRED BANQUE POPULAIRE and Managing Director of COFIBRED. Yves Jacquot is not a director of any listed company in Mauritius.

Committees:Board of Directors

Risk Committee

Corporate Governance Committee

Appointed: 23 March 2015

Qualifications:Graduate of Ecole Normale Supérieure de Cachan and University degree (Economics, Paris-I Panthéon-Sorbonne)

Henri Calvet is the founder of H2C CONSEIL, a company offering advisory and training services to credit institutions and securities firms, in the following fields: banking, accounting, prudential rules, internal control (including risk management and compliance control). Prior to setting up his own business, Henri had worked for numerous banks, BREDBANQUE POPULAIRE, Compagnie Financiere Edmond de Rothschild Banque and Compagnie Parisienne de Reescompte, inter-alia. He is not a director of any listed company in Mauritius.

Committees:Board of Directors

Risk Committee (Chairperson)

Conduct Review Committee (Chairperson)

Audit Committee (as from August 2015)

Appointed: 19 January 2009

Resigned: 28 February 2015

Qualifications:Associate of the Chartered Institute of Bankers (ACIB)

Michael joined the Hong Kong and Shanghai Banking Corporation (HSBC) in 1968 in London. He worked for HSBC for 35 years in eight different countries in Europe, the Far East, the Middle East and South America and has a wide banking experience in Corporate, Retail and Operations. He was the Head of Group Risk for the Mauritius Commercial Bank Ltd from 2005 to 2007. Michael Pike is not a Director of any listed company in Mauritius.

Committees:Board of Directors

Risk Committee

(Chairperson up to 28 February 2015)

Conduct Review Committee

(Chairperson up to 28 February 2015)

Appointed: 12 January 2007 and 13 February 2007 respectively9

Resigned: 31 December 2014

Qualifications:"Maîtrise de Gestion" from the University of Aix-Marseille III, France, graduate of "Institut Supérieur de Gestion" France, Executive Education Program at INSEAD, Fontainebleau, France and Advanced Management Program (AMP180) at Harvard Business School, Boston, USA

Born in 1968, Arnaud joined GML in 1993 as Finance and Administrative Director before becoming its Chief Executive Officer in August 2005. He participated in the National Corporate Governance Committee as a member of the Board. He is a member of the Board of Directors of several of the country's major companies and is a Director of Ireland Blyth Limited, BlueLife Ltd, LUX* Island Resorts Ltd, Phoenix Beverages Limited, The United Basalt Products Ltd, Forward Investment and Development Enterprises Ltd, Phoenix Investment Company Ltd and Alteo Ltd. Arnaud Lagesse is an ex-President of the Mauritius Chamber of Agriculture, the Mauritius Sugar Producers' Association and the Sugar Industry Pension Fund. Arnaud Lagesse is also the Chairman of GML Fondation Joseph Lagesse since July 2012. He has also recently been appointed as Chairman of the National Committee on Corporate Governance.

Committees:Board of Directors

(Chairperson up to 31 December 2014)

Corporate Governance Committee

(resigned on 31 December 2014)

Appointed: 1 September 2015

Qualifications:Bachelor of Arts (Honours):Major in History from Duke University, USA

Mark Mulroney joined the National Bank of Canada in May 2012 as Co-Head of Equity Trading and is currently the Managing Director and Head of Equity Capital Markets. Prior to joining National Bank of Canada, he worked for the Royal Bank of Canada and Goldman Sachs and Co, New York. Mark is not a director of any listed company in Mauritius.

Committees:Board of Directors

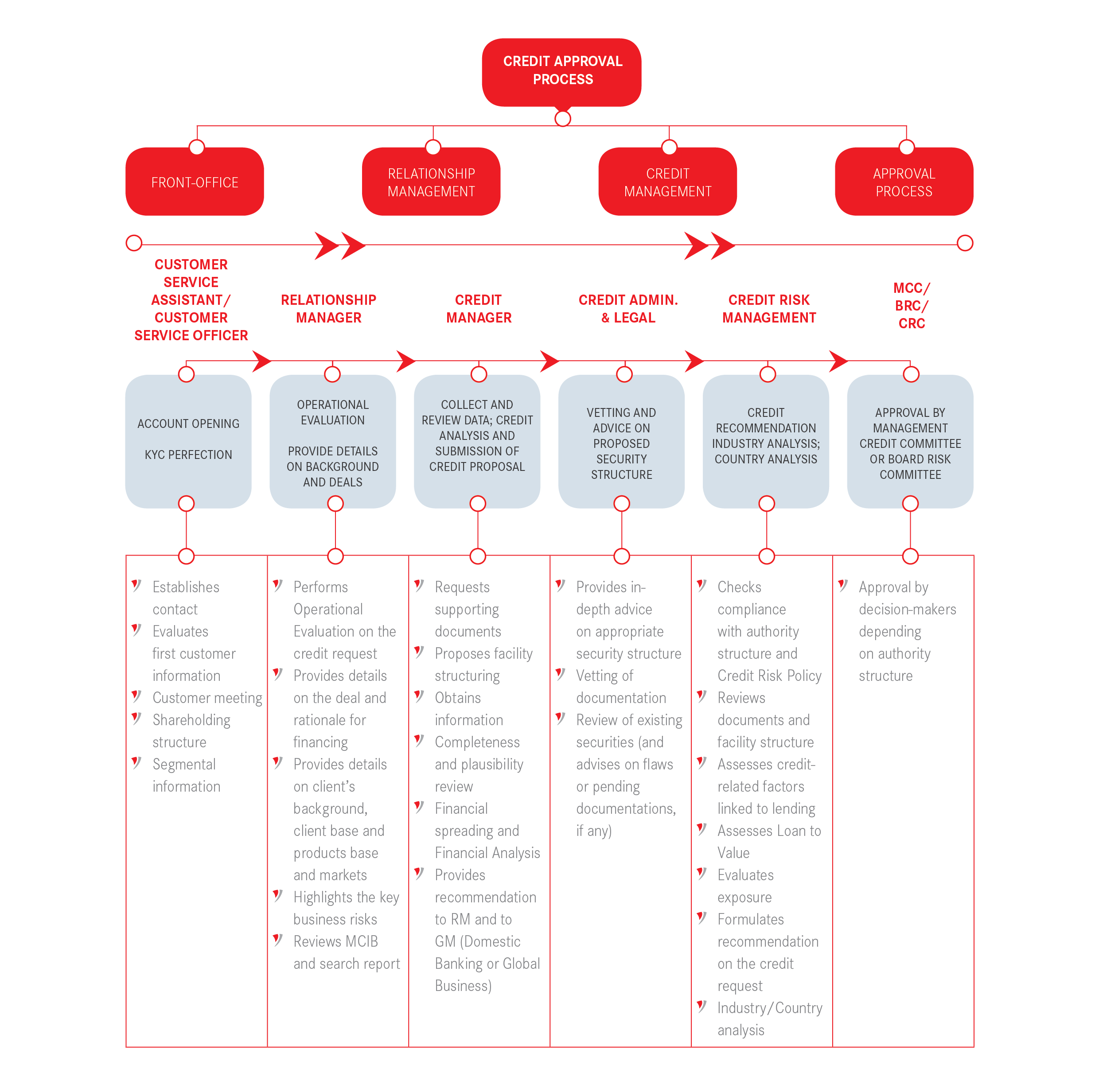

One of the key missions of AfrAsia Bank Limited (the "Bank") is to identify, assess and manage the credit, operational, market and liquidity risks to which the Bank is exposed, thereby providing a sustainable environment to attract and promote business opportunities whilst improving the risk/return profile of its activities.

Through a robust internal control mechanism, together with comprehensive and up-to-date risk policies, reliable decision making support with strict adherence to the legal and regulatory requirements, our goals remain to maintain the confidence of the stakeholders by mitigating our risk through the management of current and potential credit, operational, market and liquidity risks.

2014 elections: A landslide signaling sweeping reforms

On 17 December 2014, a new coalition Government was sworn in after winning a spectacular and unexpected landslide victory in the general elections. This brought an end to nine years of power led by the Labour Party and signaled the beginning of a new economic agenda, which was the hallmark of the electoral campaign. After months of uncertainties and stalled policy action which are often characteristics of any democratic pre-election period, the new Government took office with the promise that it would bring a "second economic miracle" to the shores of Mauritius.

Slow but gradual rebound in advanced economies...

Global growth is projected at 3.1% in 2015, marginally lower than in 2014, with a gradual pickup in advanced economies and a slowdown in emerging market and developing economies, according to the IMF. The sudden increase in financial market volatility globally in August 2015 triggered by the sharp stock market decline in China and concerns about the sustainability of its growth engine did not have long-lasting effects: financial conditions have remained favourable in advanced economies.

Global output forecasts for 2016 are expected to be lower than predicted in mid-2015 but could nevertheless strengthen to 3.6%. Recovery has been more entrenched in the United States and the United Kingdom and this is projected to increase moderately in 2016, despite fears of monetary tightening. The mild but sustained recovery in the euro area in 2015 and the return of Japan in positive growth territory are set to continue in 2016 but, according to the IMF, medium-term prospects remain subdued.

Inflation has remained on a declining trend in 2015 in advanced economies. This is expected to rise in 2016 but it is generally believed that the rates will remain below central banks' targets. In the UK in September 2015, for instance, for only the second time since 1960, the inflation rate has turned negative, reflecting a weak price backdrop. The Bank of England has warned that this could persist in 2016, thus remaining far below its target rate of 2%.

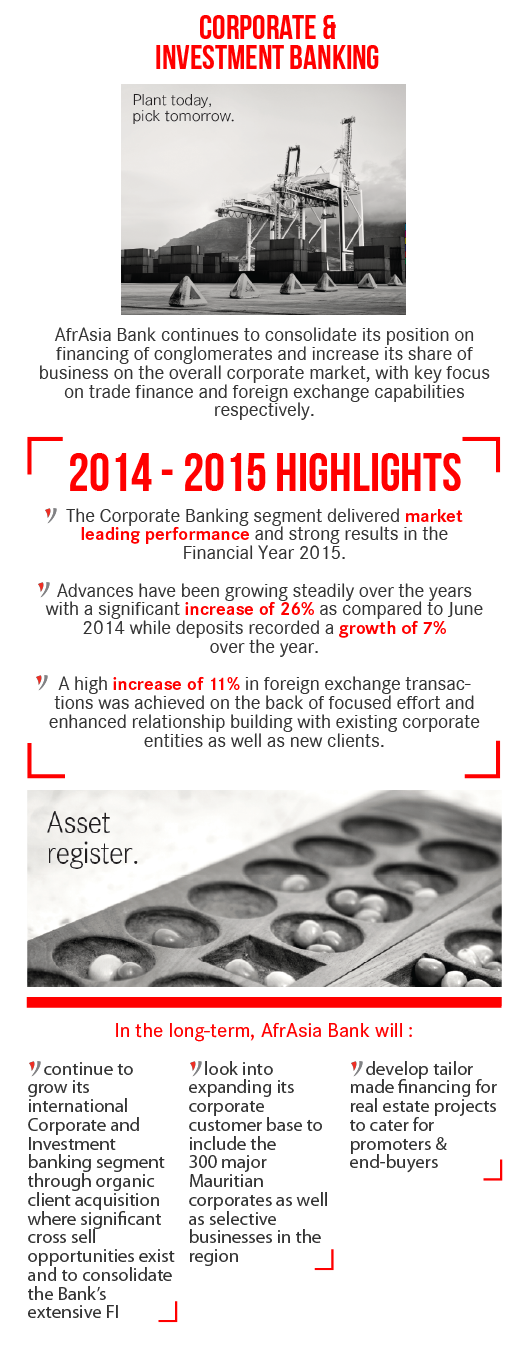

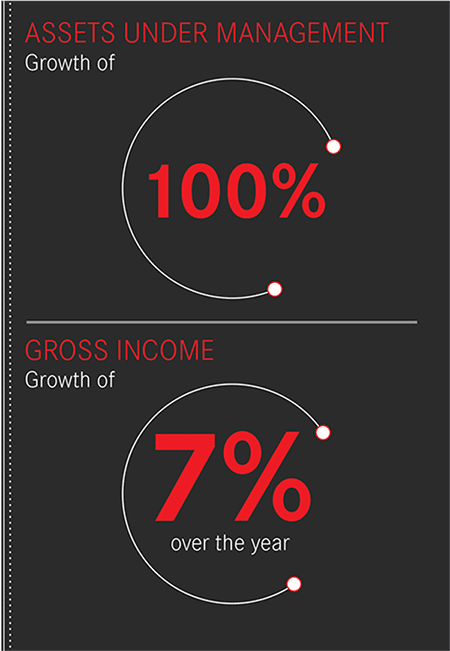

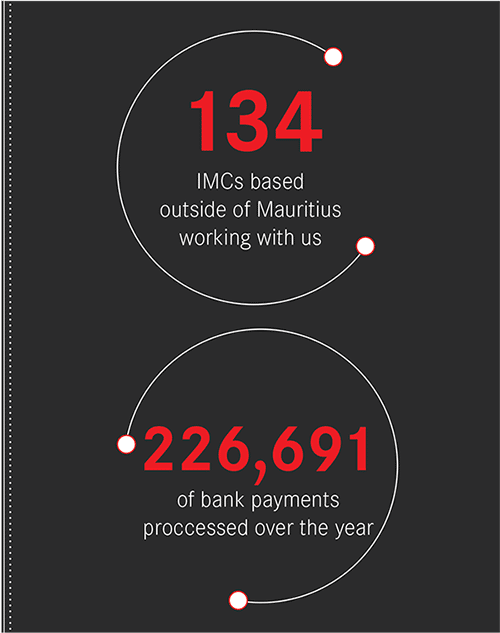

HIGHLIGHTS

|

|

HIGHLIGHTS

|

|

HIGHLIGHTSThe business opportunities have been achieved through a sustained momentum with regards to promotional and market development endeavours. Indeed, the Global Business Desk has been active in establishing and cementing the AfrAsia brand franchise during the year. The Desk made further progress in promoting AfrAsia's brand awareness on the regional and international marketplace, especially by increasing field presence, actively running business prospecting missions and road shows in targeted markets as well as participating in and sponsoring conferences. |

|

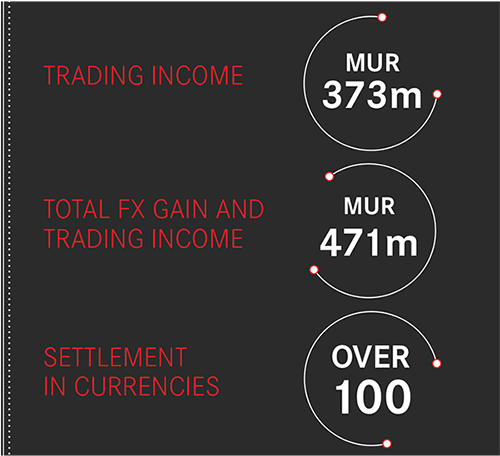

HIGHLIGHTSThe main driver was the increase in FX volumes from the Global Business segment, where the Bank witnessed a 40% increase in FX volume from FY 2013/14. The most significant increase has been on the income generated from client FX derivatives transactions which amounted to MUR 45m compared to MUR 5m in 2013/14. The Bank experienced a steady increase in its domestic banking volume to USD 1.1bn, representing a 10% increase year-on-year. |

|

Located in the two largest cities in Africa's biggest economy, Johannesburg and Cape Town, the primary functions of the South Africa Offices are to promote Mauritius as an international financial and business destination and AfrAsia Bank Limited as the banking brand of choice.

On the corporate and institutional front, South Africa remains one of the dominant investors on the Continent. According to the latest World Investment Report, South Africa recorded a 4.3% rise in FDI to USD 6.9bn during 2014, making it a leading outward investor, particularly into the rest of the African Continent. South Africa's investments into more than 40 African countries range beyond traditional mining, telecommunications, banking and travel. Other successful South African businesses with African operations are involved in insurance, construction, chemical, pay-TV, food and beverage as well as the pharmaceutical sectors. Every year growing numbers of African consumers shop at South African retailers such as Shoprite or Massmart stores. Many of these companies engaged in trading in Africa have invested via Mauritius – or use Mauritius as an international treasury centre.

According to New World Wealth's Africa 2015 Wealth Report, the number of HNWIs in Africa increased by 145% between 2000-2014, comparing very favorably with the worldwide HNWI growth rate of 73% during the same period. Moreover, these numbers are expected to rise by a further 45% by 2024. Clearly there is a correlation between economic growth and the creation of a successful and wealthy entrepreneurial class. With the African Continent set to become one of the world's fastest growing regions over the next 10 years, there will be a concomitant rise in the demand for banking and investment products and services which augurs well for those providing private banking to the African clientele.

The Representative Offices have been capitalising on 3 main trends:

The Representative Offices' local presence combines well with the Bank's competitive products and services enabling AfrAsia Bank Limited to successfully compete for international banking in the markets in which it operates.

Since inception, the strategy has been to retain the services of seasoned bankers who are well grounded in the local market and also have the ability to inform prospects about international banking through Mauritius. This ranges from being able to discuss with global business companies as well as speaking to individuals about the private banking platform in Mauritius.

Tangible and intangible benefits accrue to positioning ourselves in one of Africa's largest economies.

Each year, the South African Representative Offices continue to contribute to the Bank's expansion into African and other markets.

The team in South Africa. From left to right; Ravi Teji, Vanessa Sabbatini (consultant), Colin Grieve, Anne Ferriera, Lise Tayler and Dennis Shoko

The Bank's presence in London reflects the city's importance as a centre for African-focused capital flows. It is also home to a large proportion of the major African private equity groups and our London Representative, Garry Sharp, himself has deep experience in African private equity stretching back nearly twenty years.

The key role of the Representative Office is to act as a networking and contact centre, enhancing our relationships with London financial institutions, advisers and intermediaries, and with clients and contacts who pass through the city. The Bank also liaises closely with the London offices of Mauritius-based management companies and similar partners.

Key achievements in the last twelve months have included:

The Financial Year 2014/15 was marked by the closure of the Bank’s Zimbabwe operations, despite all efforts made to salvage them. This happened against the backdrop of deteriorating macroeconomic conditions and a continued liquidity crunch in the banking sector.

In February 2015, the board of AfrAsia Bank Zimbabwe Limited (ABZL) decided to surrender its banking licence. Despite the writeoff of this investment, AfrAsia Bank Limited continues to maintain a strong capital based of MUR 4.9bn, demonstrating the resilience and financial strength of the Bank.

AfrAsia Corporate Finance (ACF) is a niche, independent corporate finance adviser; providing clients with innovative structuring and financial solutions. The AfrAsia Corporate Finance Team based in Johannesburg, South Africa, consists of Marisa Meyer and Llewellyn Gerber; together they bring nearly three decades of experience.

Collectively, Marisa and Llewellyn have broad and deep experience in a variety of disciplines, ranging from Investment banking, Capital Raise and Tax Advisory to Debt Capital Markets, Valuations and Fairness Opinions as well as M&A advisory.

ACF has been instrumental in prepping, executing and delivering on many strategic and multifaceted business transactions. Their approach to partner with their clients rather than acting solely as advisors, coupled with their experience, connections and skillset, means they are able to provide their clients across the African continent with a range of appropriate solutions, all the while offering them the satisfaction that all their business requirements will be met.

Long-Term Financing

Most Preferred Employer

Children's Education

AfrAsia Green Programme

AfrAsia Bank Mauritius Open 2015

AfrAsia Bank Mauritius Open, the first ever tri-sanctioned golf tournament endorsed by the Sunshine, European and Asian Tours, all of whom are founding members of the International Federation of PGA Tours, was held at the Heritage Golf Club. George Coetzee was crowned winner of this inaugural tournament.

AfrAsia Bank Cape Wine Auction 2015

The AfrAsia Bank Cape Wine Auction, held in Boschendal (Cape Town) raised an astounding ZAR 10.5m for children's education in South Africa's winelands.

Brand Ambassadors: Hennie Otto and Max Orrin

The Bank has signed a sponsorship agreement with the young and talented English golfer Max Orrin, winner of the 2014 AfrAsia Golf Masters as well as a personal endorsement deal with three-time European Tour Champion Hennie Otto.

AfrAsia International 7's Rugby Tournament

The Bank, in collaboration with Rugby Union Mauritius, organised the 2nd edition of AfrAsia International 7's Rugby Tournament at the Northfields Sports Club, Mauritius. The Outeniqua team from South Africa were crowned as winners.

Sponsor of 2014 Derby Golf de Guérande, France

The Bank sponsored Golf de Guérande's inaugural Derby Golf 2014, a 36-hole stroke play event played over two days, witnesssing the participation of 120 golfers.

Africa Pensions and Sovereign Investment Forum 2014, London, United Kingdom

AfrAsia Head of Private Equity and London Representative Office Garry Sharp was a key speaker at the Forum, and focused on future challenges of doing business in the African market.

Offshore Bootcamp sponsored and co-hosted by AfrAsia Bank, Cape Town, South Africa

Ryan De Vries, AfrAsia Bank Cape Town Business Head and South Africa Chief Representative Officer Colin Grieve spoke about international banking, Foreign Account Tax Compliance Act and future automatic exchange of information agreements.

Private Equity in Emerging Markets 2014, London,United Kingdom

AfrAsia Head of Private Equity and London Representative Office Garry Sharp attended the conference focusing on latest developments in the asset class and emerging economies.

Annual Super Return Africa 2014, Cape Town, South Africa

Our team attended the conference, focusing on the opportunities and challenges of investing in private equity across Africa.

Africa Financial Services Investment Conference, Brighton,United Kingdom

Garry Sharp, Head of Private Equity of AfrAsia Bank Limited, was a speaker at the conference, focusing on "Private Equity and Financial Services: Pointers from a Busy Year."

Launch of Ebène digital flagship branch

AfrAsia Bank Limited opened its conceptual branch in the Ebène CyberCity, showing its continued growth and development of the brand, delivering simultaneously a distinctive customer experience through the I-Displays, I-Tables and the 84" I-Wall, a first in Sub-Saharan Africa.

AfrAsia Tecoma Award 2014

The Bank sponsored the AfrAsia Tecoma Award for the third time, honouring the best of the local business community whose courage, foresight and determination has created and sustained successful, growing business ventures. Aisha Allee from Blast Communications became the first woman to be honoured with this recognition.

We have audited the consolidated and separate financial statements of AfrAsia Bank Limited (the “Bank”), which comprise the statements of financial position as at 30 June 2015 and the statements of profi t or loss and other comprehensive income, changes in equity and cash flows for the year then ended, and the notes to the financial statements which include a summary of significant accounting policies and other explanatory notes, as set out on pages 186 to 307.

This report is made solely to the Bank’s members, as a body, in accordance with Section 205 of the Mauritius Companies Act. Our audit work has been undertaken so that we might state to the Bank’s members those matters that we are required to state to them in an auditors’ report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Bank and the Bank’s members, as a body, for our audit work, for this report, or for the opinions we have formed.

LIM SIT CHEN LAM PAK NG

Chairperson

JEAN DE FONDAUMIERE

Director

CATHERINE MCILRAITH

Director